The geopolitical and economic uncertainty that has gripped the world since the election ofDonald Trump has now had its counterpart in the financial markets. Interest rates are rising in Switzerland (after falling in 2024), pushing bonds down but property and equities up. Growth stocks are falling, while value stocks are rising. Gold is climbing, while crypto-currencies are tumbling. The pitfalls are multiplying in a disorderly market, and investors are having to navigate a complex environment.

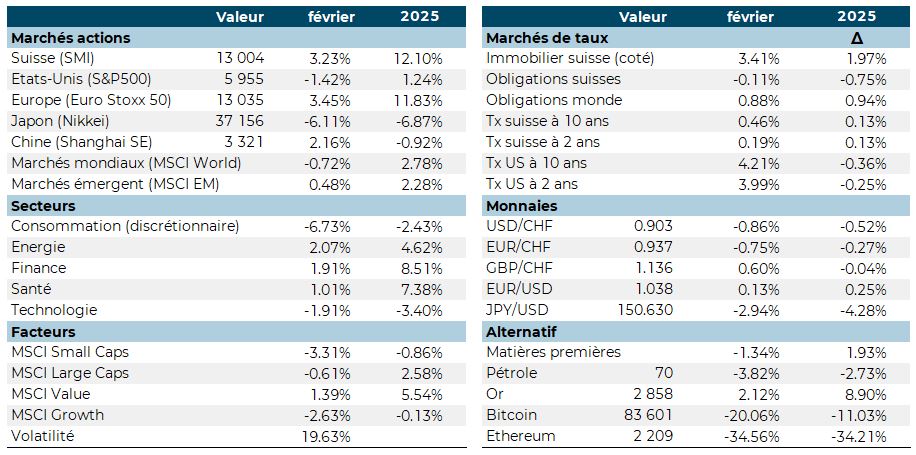

Equity markets have seen contrasting performances, with European and Swiss indices making clear gains, while US and Asian markets are under pressure. Technology stocks fell for the second month running.

Interest rates moved differently from region to region, impacting bond markets unevenly, with global bonds up 0.9% over the month. Swiss property prices rose sharply after a negative January.

The USD and EUR were down against the CHF. The JPY fell sharply against the USD. In alternative assets, commodities fell back and gold continued its good start to the year.

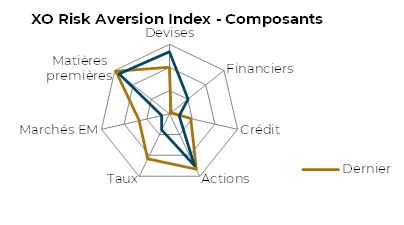

The fall in the risk indicator was wiped out in the last few days of the month as emerging market and interest rate risk indicators rose.

Main Performances February

XO Risk Aversion Index - Composite 250D

XO Risk Aversion Index - Componants

January

Economic Review

Growth in sight in the United States and gloom in Europe

Donald Trump is giving his instructions this January: lower oil prices, lower US interest rates. Unfortunately, neither seems to be responding to his demands. With inflation picking up slightly (2.9% in December), the FED is putting on hold the cycle of rate cuts that began in September. Powell cites domestic political uncertainty as one of the reasons for the pause. If the tariff barriers imposed on Canada, Mexico and China were to rise, excess inflation of between 0.5% and 2% could emerge. If the tariff barriers imposed on Canada, Mexico and China were to rise, excess inflation of between 0.5% and 2% could emerge. And the slowdown in wage growth offers a counterbalance to the impact of the tariffs.

Philadephia Fed Business Outlook

Donald Trump is giving his instructions this January: lower oil prices, lower US interest rates. Unfortunately, neither seems to be responding to his demands. With inflation picking up slightly (2.9% in December), the FED is putting on hold the cycle of rate cuts that began in September. Powell cites domestic political uncertainty as one of the reasons for the pause. If the tariff barriers imposed on Canada, Mexico and China were to rise, excess inflation of between 0.5% and 2% could emerge. If the tariff barriers imposed on Canada, Mexico and China were to rise, excess inflation of between 0.5% and 2% could emerge. If the tariff barriers imposed on Canada, Mexico and China were to rise, excess inflation of between 0.5% and 2% could emerge. And the slowdown in wage growth offers a counterbalance to the impact of the tariffs.