De-dollarisation

The decline of the USD since the beginning of the year and the emergence of exchange solutions by the BRICS may mark the coming de-dollarisation of the world economy

USD under pressure

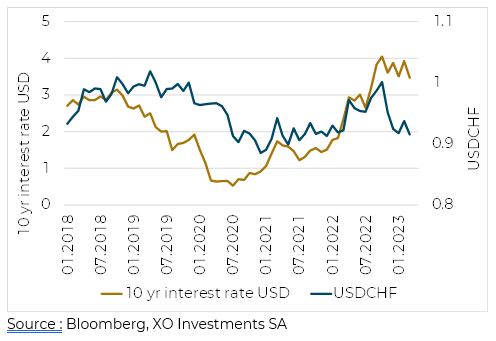

The end of 2021 and the first ten months of 2022 were dominated by the USD. With inflation accelerating, the Federal Reserve (FED) used the main tool at its disposal to reduce inflationary pressure: interest rates. With a massive and rapid rise in rates over a year, the immediate consequence was a rise in the USD against the major currencies. Over this period, the rise of the USD against the CHF was over 10%. High interest rates make a currency more attractive.

But since November 2022, inflation has been slowing down. Economic players are anticipating a possible change in US monetary policy and thus an end to the rise in interest rates. Accordingly, US 10-year rates have stagnated for several months at a level slightly below 4%. The corollary of this new situation is that it reduces the interest in holding the USD. And so, naturally, the USD is starting to fall. Against the CHF, it is already down 4% over 2023, with a low point in April below the 0.89 threshold. Since the beginning of November 2022, the decline has even been more than 10%.

Evolution USD and USD rate (%)

A decrease in value but a constant value in trade

This current downward trend in the USD is linked to interest rates, but the value of the USD has been falling continuously since 1971. For the USD against the CHF, as for the majority of reference currencies, it is 80% down in 50 years.

1971 corresponds to the end of the Bretton Woods Agreement (1944) with the end of the gold convertibility of the USD. The main reason for this change was the possibility of creating money without any constraint, and thus increasing the level of debt of the American State to finance the Vietnam War.

Evolution USD/CHF

A de facto USD standard was created in 1971, or rather petrodollar. This monetary system had been constructed in 1945 by President Roosevelt in an 'oil for security' agreement with Saudi Arabia. The abandonment of the gold exchange standard allowed the US to become totally dominant on the international scene thanks to its currency.

The decline in the attractiveness of the USD is also reflected in the reserves held in USD by the main central banks. In 25 years, central bankers have held 12% less in USD, a sign of a greater aversion to the greenback.

Réserves in USD in %

Despite this decline and the loss in value of the purchasing power of the USD against the major international currencies, the USD remains the main currency reserve ahead of the EUR.

Foreign currency reserves (EUR and USD) in %

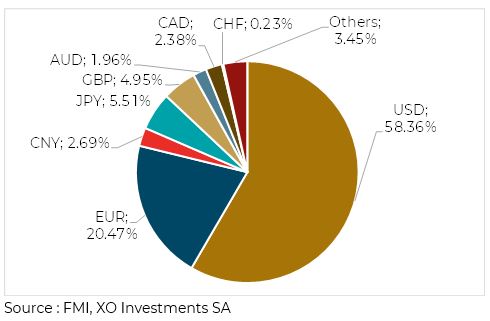

The international role of the US currency remains high, as almost 90% of global currency trade is still conducted in USD. Almost 50% of cross-border lending of international debt securities is in USD. 50% of commercial invoicing and over 42% of international SWIFT payments are in USD.

Rôle international de l'USD International role of the USD

The rise of the BRICS

However, the world has been changing in recent years with the impetus of the BRICS countries (emerging countries such as Brazil, Russia, India, China,...).

Foreign exchange reserves

Indeed, although they represent little in terms of global foreign exchange reserves, trade is growing.

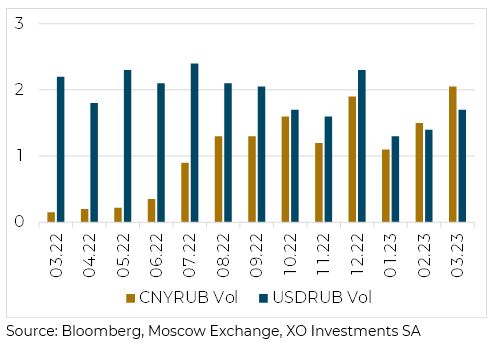

The war in Ukraine is obviously an accelerator of this phenomenon. The freezing of the Russian central bank's assets led Russia to impose the sale of its oil and gas in roubles. The effect is immediate as the volume of trade in rouble-yuan has just exceeded the volume of trade in rouble-USD

Currency trading volume (USD trillion)

The BRICS countries have just overtaken the G7 in terms of GDP (31.5% of world GDP against 30.7%). They are gradually introducing trade in their national currencies outside the dollar for their bilateral trade: Russia and China, recently Brazil and China. The BRICS are working on the creation of a new financial instrument by seeking to create an international exchange currency based on their national currency and several raw materials. Countries are commencing to act geopolitically without "referring" to the former world policeman, the United States: Iran and Saudi Arabia are renewing diplomatic relations, China is acting to put an end to the Ukrainian conflict, etc.

Vers une dédollarisation progressive Towards a progressive de-dollarisation

De-dollarisation seems to be underway. But it will take time. One currency will not replace the other and each state has an interest in the system sliding gradually and not abruptly. The effects will nevertheless be multiple, both geopolitically and economically, with a rebalancing, inflationary problems or the localisation of industries.

These other articles may also interest you