Heterogeneite of pension fund votes

delegation of pension fund votes at general meetings to financial service providers results in significant dispersion and sometimes leads to incongruities

In 2013 the Swiss voted in favour of the Minder initiative against abusive remuneration. This initiative had an immediate impact on pension funds, which must now express their opinions at the general meetings of listed companies, particularly Swiss companies. Pension funds must vote in the interest of their policyholders and justify their decisions, for example in their annual report. For this purpose, pension funds define the modus operandi in specific guidelines. Investing through investment funds and foundations relieves pension funds of this administrative burden. By delegating the management to funds and foundations, the voting is also delegated to the asset manager.

XO Investments systematically collects the votes of several financial providers in order to analyse and consolidate them on behalf of its clients. Thanks to this expertise, we are able to analyse the voting behavior of three asset managers often employed by pension funds. For confidentiality reasons we will call them AM1, AM2 and AM3. In order to restrict the universe, we focus on SMI stocks and the period 2021-2022. This sample represents more than 3'000 votes!

Different votes between managers

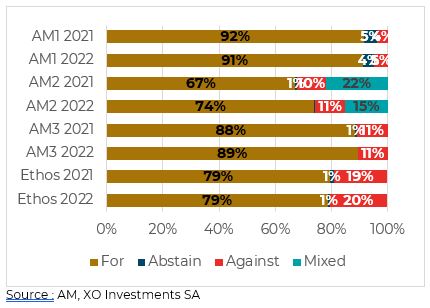

First, we simply analyse whether the proposals put to the vote are accepted or rejected by the financial provider, or whether the provider abstains from voting. The first two charts show the votes of the three asset managers for 2021 and 2022. The vast majority of the items voted on are supported by the voters. Although not statistically significant, there is an increase over the period in votes in favour and a decrease in abstentions.

To obtain a form of benchmark, we also use the recommendations of the Ethos company. In the context of this study, we therefore consider that Ethos' exercise of voting rights optimally represents the interests of Swiss pension fund members. In a global comparison, Ethos is opposed more often than the asset managers we consider, a difference of almost 10%. Asset Manager 1 (AM1) differs the most from Ethos in terms of votes.

Distribution of votes by managers

Distrust of management

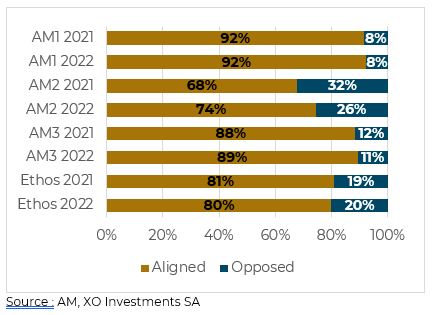

The second part of our study leads us to analyse the alignment of votes with management, i.e. with the proposals made by management and the board. According to our data, AM1 is most often in agreement with the proposals made by the boards, followed by AM3 with almost one vote in ten against the management's recommendations.

Surprisingly, AM2 seems to go against management much more often. It should also be noted that this asset manager does not vote uniformly for all the funds for which it represents the votes. Thus, for a given general meeting, on a specific voting item, AM2 may express different and sometimes even contradictory votes between its funds. In our sample and for the period under review, AM2 is different from its peers with a more negative vote towards management than the other companies.

In general, we note a certain difference between the behaviour of the providers and that of Ethos. Indeed, the service providers we analyse more often follow management's recommendations than Ethos.

Alignment of votes with management

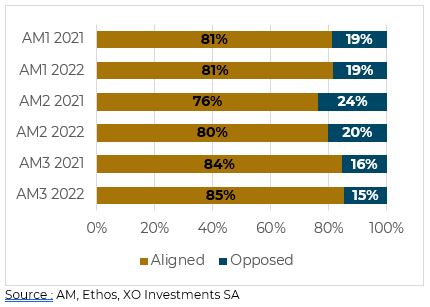

To go further, we compare the managers' votes against Ethos' voting proposal for each proposal submitted to the vote at the general meetings. The analysis of the results shows that AM3 is the manager who votes most often in the interest of the policyholders, as measured by Ethos' proposals. Indeed, about 85% of the votes of AM3 are identical to Ethos' proposals. In second place comes AM1 with identical votes in 81% of cases. Finally we find AM2 with between 75% and 80% identical votes for 2021 and 2022 respectively. Finally, over the period under review, the percentage of identical votes to Ethos' increases for all asset managers.

Alignment of votes with Ethos

The tug of war between Ethos and management

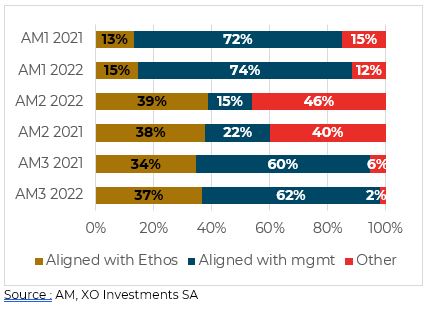

When Ethos and management give divergent recommendations, how do asset managers behave? The graph below allows us to answer this question. The graph shows the voting behavior of financial service providers when there is a difference between the voting recommendation given by management and that given by Ethos.

Voting behavior in case of divergence between management and Ethos

In general, it seems that financial providers tend to follow management when there is a conflict between Ethos and management. Indeed, AM1 and AM2 follow management in more than 60% and 70% of cases, respectively. For AM2, the conclusion is not as clear-cut, as the service provider votes differently for about 40% of the votes.

Despite this tendency to follow the management, we notice once again a different behavior between providers. Indeed, Ethos' recommendations are followed by AM2 and AM3 in more than a third of the conflicts. This percentage is significantly lower for AM1, which follows Ethos' recommendations in only 13% of conflicts.

No Uniformity in compagnies

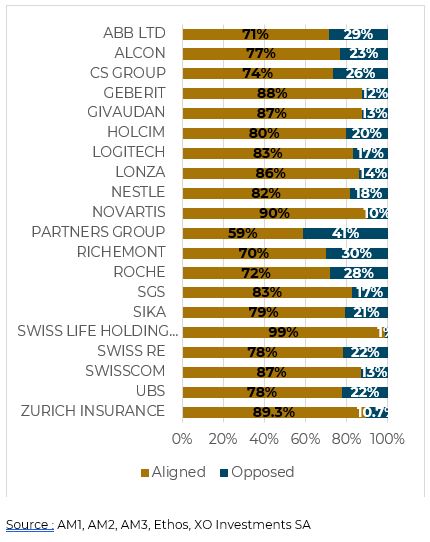

The last step of our analysis consists in presenting the votes by company to check whether the results presented above are attributable to certain companies. We therefore measured the alignment between asset managers' votes and Ethos' recommendations for each company. The votes of the different financial service providers are aggregated.

The first observation is that the alignment is obviously very different from one company to another. For example, in 2021, the votes of the three providers at Swiss Life's meetings were 99% in line with Ethos' recommendations. At the other end of the spectrum is Partners Group, where only 59% of Ethos' recommendations were followed. The spectrum is therefore very broad, but the alignment is between 76% and 81% for half of the SMI companies.

A company's sector of activity does not seem to be a determining factor for alignment with Ethos. Indeed, financial and pharmaceutical companies are found at both extremes, such as Roche, with only 72% alignment.

Alignment of votes by company, 2021

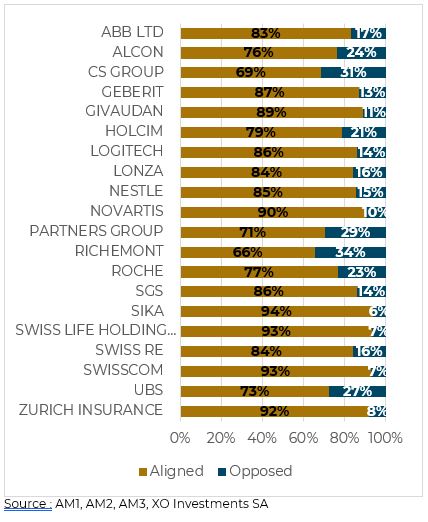

The second finding is that alignment at the company level is relatively stable over the two years under consideration. Asset managers therefore tend to follow, or not follow, Ethos' voting proposals for the same companies. The three asset managers under review have a low alignment with Ethos' voting recommendations for the following three companies: Partners Group, Richemont and Credit Suisse. Similarly, at the general meetings of Swiss Life, Swisscom and Zurich, the asset managers have a high alignment with Ethos' voting recommendations in both periods under review.

We also note that listed financial service providers can vote at their own general meetings and at those of competitors. At these meetings they can exercise voting rights for all shares held in the fund. Governance can therefore quickly reach its limits. Perhaps constraints could be considered in the future in order to guarantee complete independence and neutrality in the expression of votes in the service of pension funds and policyholders.

Alignment of votes by company, 2022

The GSS at the heart of the LPP

The introduction of voting within investment funds and foundations available to pension funds facilitates the work of pension funds. The ESG reporting standard published by ASIP in December 2022 calls for BVG players to take more interest in how their selected managers vote at general meetings. Each provider has its own behaviour which leads to votes that can be diametrically opposed, sometimes within the same institution between two of its products. A lot of governance work remains to be done if institutions are to have full control over the destiny of their policyholders.

The governance often mentioned by pension funds requires transparency and reflection on the subject of voting at general meetings. But it is also essential to limit the administrative impact of such analyses for pension funds. One of the first steps could be for XO Investments to carry out a similar study annually. This would allow pension funds to choose their providers not only on the basis of fees or the quality of their management, which are generally closed for passive investments mainly used by funds, but also on the way they apply the principles of good governance, on voting at general meetings or on the consistency of their approach.

These other articles may also interest you