Market Review September

Flattening the curve

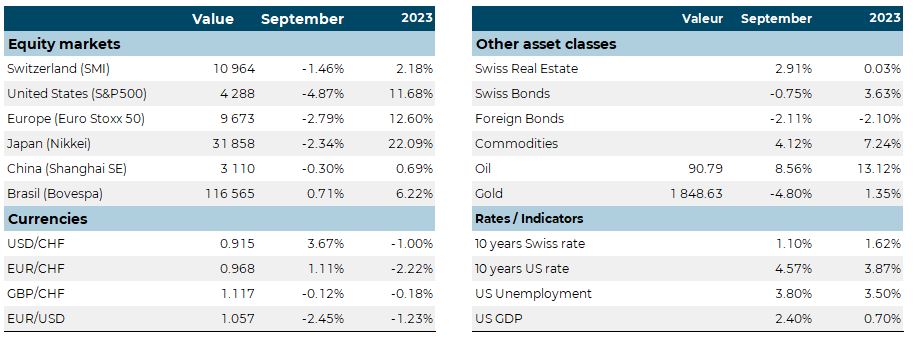

The main central banks met in September. Their rhetoric was relatively similar, as they raised interest rates and warned of a halt to rate rises. With inflation under control, a period of higher but stable rates seems to be in store for the coming months, both in the US and in Europe. In Switzerland, too, the mood is calmer, suggesting some easing in long-term rates. The consequence of this is a flattening of the yield curve, i.e. short-term rates at the level of long-term rates.

Bonds have been affected by this latest upward movement, moving into negative territory overall since the start of the year. Real estate is recovering after a difficult few months. Equities were under pressure throughout September. The United States was the worst-affected market, led by a technology sector that corrected significantly.

The USD and EUR rebounded strongly against the CHF following central bank statements. Oil continues to advance, while precious metals are suffering from the strength of the US dollar.

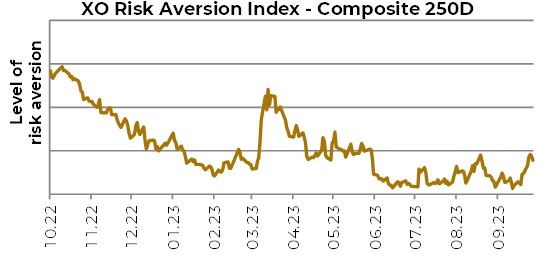

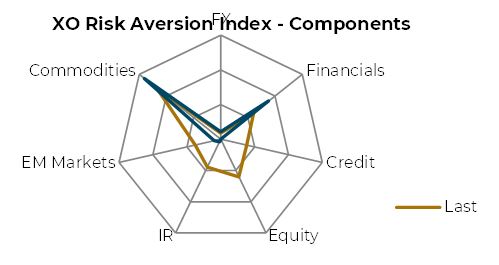

As last month, the risk indicator is very low, except for commodities.

MAIN performances

XO Risk Aversion Index - Composite 250D

XO Risk Aversion Index - Components

These other articles may also interest you