Pension Funds at the forefront of private wealth management

on the strength of the rigour with which they manage their assets, pension funds and the methods they use, in particular ALM, could assist private wealth management in defining client risk profiles.

Determining a performance requirement

Early autumn is traditionally the time when rates or increases applicable from 1 January are announced: health insurance premiums, energy prices, etc. This is also the case for pension fund rates such as the minimum BVG/LPP interest rate. This is also the case for pension fund rates, such as the minimum BVG/LPP interest rate. This is a rate that reflects ambitions for the profitability of pension assets.

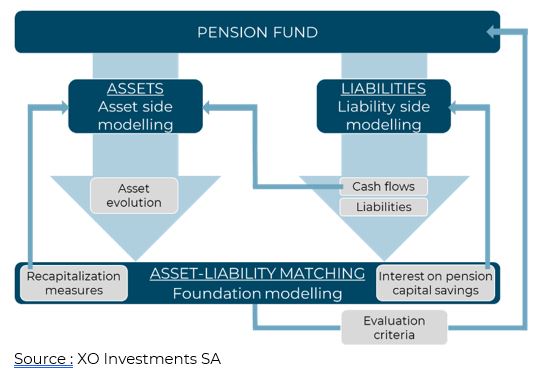

The rise in interest rates has had a major impact on pension funds. As part of their governance process, many of them have re-examined their return requirements for 2023 in order to determine their profitability targets. This profitability target then defines their strategic allocation, i.e. the way in which they will allocate their capital between equities, bonds, property, etc. This is what is commonly known as ALM (Asset and Liability Management) or Asset-Liability Congruence.

ALM Methodology

This ALM study is carried out regularly by pension funds. It makes a number of assumptions about the liabilities side of the balance sheet: changes in the workforce, turnover rates, salary trends, capital take-up rates, probability of retirement at age 61 or 62, etc.

There are many lessons to be learned from this study of the first simulations of the workforce (and therefore of balance sheet liabilities). Cash flows (annuity payments, contributions received, etc.), for example, provide a tool for managing liquidity.

Cash flow

The fund's performance needs are also estimated. This is the result of a number of factors: the level of interest rates paid to policyholders, the profitability promised to pensioners, the cost of longevity, etc.

Need for performance

Allocation at the heart of the objective

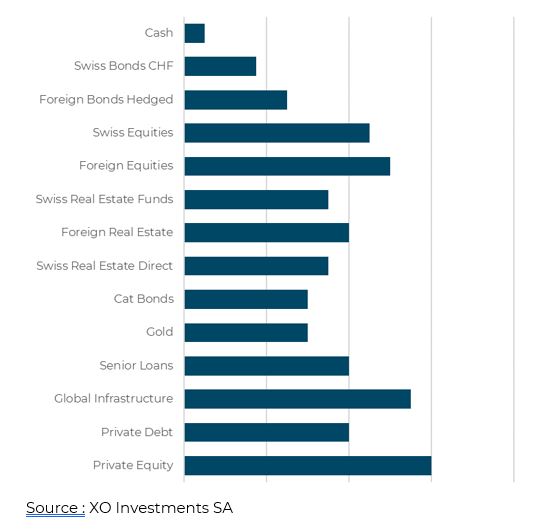

The second part of the ALM analysis focuses on the assets side of the balance sheet, i.e. investments. Here, too, the assumptions are numerous and relate mainly to the profitability of the asset classes and their behaviour (volatility, for example).

The pension fund's asset allocation, i.e. the composition of its investments, makes it possible to determine an expected return, which needs to be compared with the performance requirement determined above.

Expected return on asset classes

The objective of an ALM is therefore to match the return required to meet the fund's commitments (liabilities) with the expected return on investments (assets). This congruence between the two sides of the pension fund's balance sheet is the search for a multiple balance: generational, assets-pensioners, and of course in terms of risks (disability/death, financial risk, etc.).

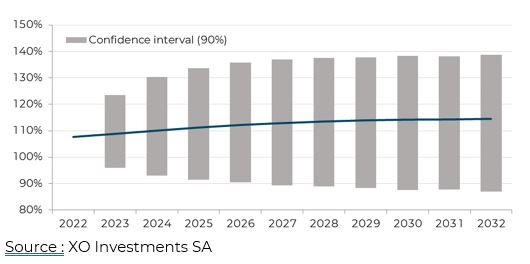

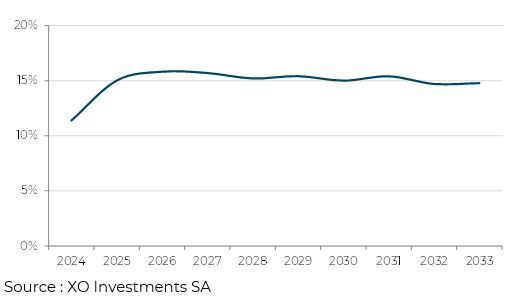

Taking into account the pension fund's investment strategy, it is possible to simulate its behaviour in the face of events and the assumptions made. Thousands of scenarios can be constructed. This set of trajectories can be used to determine the potential path of the pension fund. The degree of cover can also be estimated for the coming years. It is interesting to note a variability in the possibilities that tends to reduce over time.

Change in the funding-ratio

A probability of under-coverage can also be determined. In the example given, it is 12% over one year, 16% over two years, and then this statistic stabilises. Here again, the investment horizon is decisive when defining the foundation's asset allocation.

Probability of under-funding

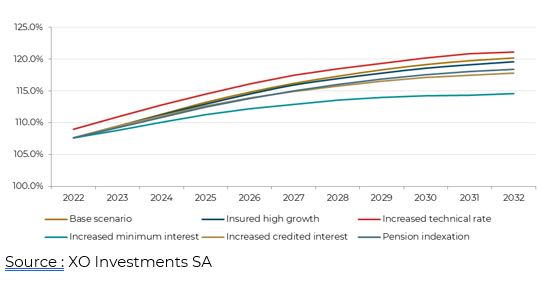

The degree of cover will be influenced by the fund's major decisions or by changes in the basic assumptions used. For example, an increase in the technical rate tends to improve the cover ratio, as does an increase in the number of employees.

Changes in the level of funding ratio

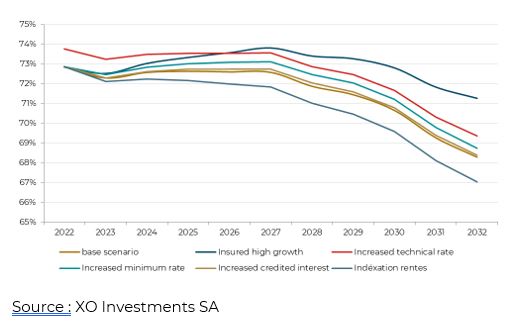

The structure of the fund can be greatly affected by the choice of certain parameters, for example the choice of the technical rate, which can change the ratio of liabilities to pensioners in the liabilities side of the balance sheet.

Active insured ratio

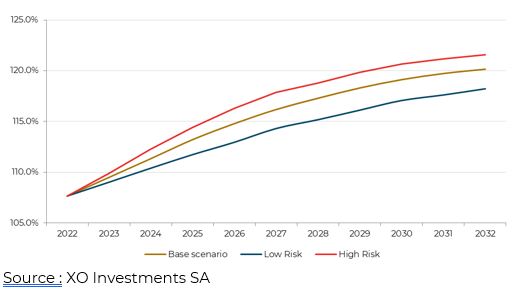

Le dernier travail de l’ALM a trait à la recherche d’une amélioration de la structure des placements, soit une optimisation de l’allocation d’actifs. En fonction du risque pris le degré de couverture sera là aussi influencé.

Change in the level of cover

ALM as a risk profile tool

The introduction of the LSFin and LEFin on 1 January 2020 marks a turning point for asset management in Switzerland. Regulatory constraints are becoming more stringent, and banks and independent asset managers will have to be more diligent and structured in the services they offer clients. In particular, defining a risk profile for a private client requires more in-depth questionnaires and more frequent reviews.

It is not easy to define a risk profile for a private client. Recent financial theory makes it possible to use behavioural finance as a basis for reflection, but questionnaires of this type are sometimes rather long and difficult for customers to understand. The methodologies used by pension funds, in particular ALM, could prove a great help in determining a client's risk capacity.

Some clients are able to define a "return requirement". This need can be used to propose a strategic allocation. It remains to be seen whether this need for return is consistent and does not imply an excessive risk in a particular situation (for example, a pensioner who believes he needs to earn 10% a year to maintain his previous standard of living).

A relatively easy way of starting a discussion on the risk profile is to simulate the asset allocation

envisaged and share the conclusions in terms of risk with the client. This amounts to presenting simulations of the strategy in the same way as for an ALM.

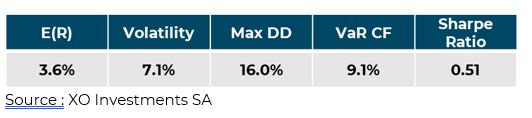

The asset allocation defined in this way provides the investor with return and risk characteristics such as expected return, losses over a certain period or the risk (volatility) of the portfolio.

Losses (Drawdown)

Example of portfolio statistics

The customer can also determine the probability of potential but not maximum loss (VaR), which is used by pension funds to set fluctuation reserves. If the customer believes that the potential loss over a year is too great, a less risky strategy should be chosen.

All these risk parameters, derived from the methodology used by pension funds, could therefore form the basis for defining the risk profile of a private client.

20 years ago, the financial sector contrasted wealth management for private clients with so-called institutional management for pension funds. The training and profiles of the people working in these two areas were different, as were the themes addressed and the products used. This is much less true today. A convergence of ideas and methods is taking place, and private wealth management, even though it is more than two hundred years old in

These other articles may also interest you