Precious Metals : Everyone talks about them but nobody has any

Gold is shining brightly, accompanied by silver and gold miners, and favoured by asians, it nevertheless remains low in investirs' portfolios

New records

Gold, sometimes referred to as the barbaric relic, has been at the forefront of the financial scene in recent weeks. The war in Israel acted as a detonator for an asset that had remained relatively stable since 2020. This stability already spoke volumes about its underlying strength, as the unfavourable environment (rising interest rates) had had little impact. Records have been falling every week since 1 March. An Olympic year may be on the horizon.

Gold price (once in USD) since 2020

Gold smashed its all-time record to reach USD 2,400/ounce in April, rising by almost USD 400, or 20%, since 1 March.

Gold price (once in USD)

The movement in gold has been accompanied by a rise in assets similar to or linked to the yellow metal, namely silver and gold mines.

Silver has risen in the same proportion as gold if we compare it since 2020. For gold mines, even though 2024 was a very profitable year, they are still more than 30% behind the rise that began in 2020.

Gold, silver and gold mines since 2020

Looking at longer time scales, the behaviour of these assets is interesting. Both gold and silver act like leveraged assets, moving up and down violently.

Gold is beating its all-time high, which is not the case for silver or the gold mining index. Silver is at around 50% of its all-time high, while the gold mining index is only worth a third of its 2011 high. There is still a long way to go.

Gold, silver and gold mines since 2001

Nonetheless, a higher gold price will mean better revenues for mining companies, and a recovery phase can then begin.

Asian flows

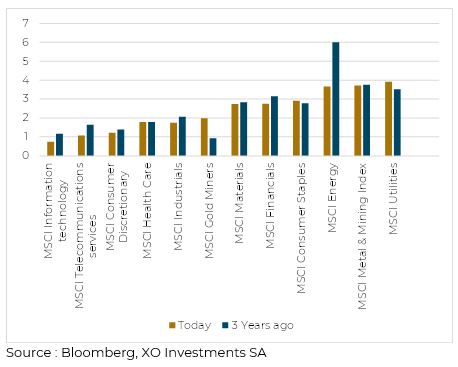

The recent rise has several origins. Expectations of a rate cut at the end of last year gave gold assets a major boost. These are mines that now offer a relatively attractive dividend yield, much higher than that of technology or service companies.

Dividend yield (%)

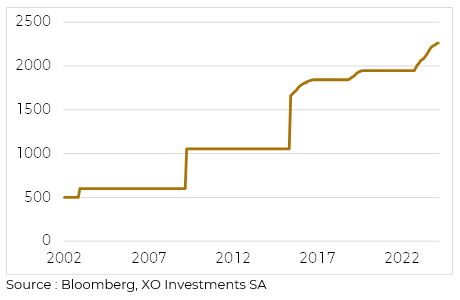

The war in Ukraine, the expansion of the BRICS and their desire to give their currencies credibility in international trade are also key factors in gold buying. Some central banks have clearly stated their desire to link their currencies to tangible assets such as gold. This is the case with Russia. China does not communicate much, but its actions speak for themselves. This is the 17th consecutive month that China has bought gold, thereby increasing its reserves. They now stand at 2,262 tonnes, making it the 7th largest holder after Russia.

China's gold reserves (tonnes)

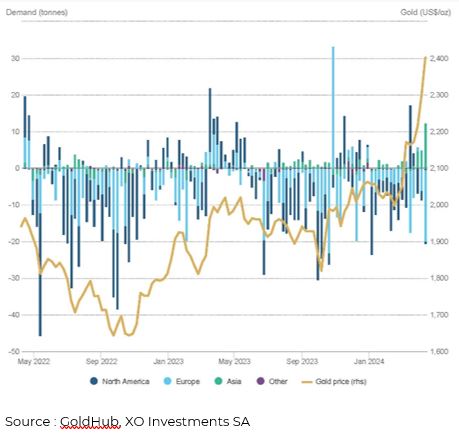

In Asia, it's not just central banks that are buying gold; investors seem to have been flocking to these assets in recent weeks.

Average flow over 4 weeks in the Huaan Yifu Gold ETF (millions CNY)

One example is the Huaan Yifu Gold ETF, which has accounted for the most flows over this period, with almost 2 tonnes since the start of the year. Weekly withdrawals in Europe and the United States are now more than offset by inflows from Asia.

Weekly flows by regions (tonnes)

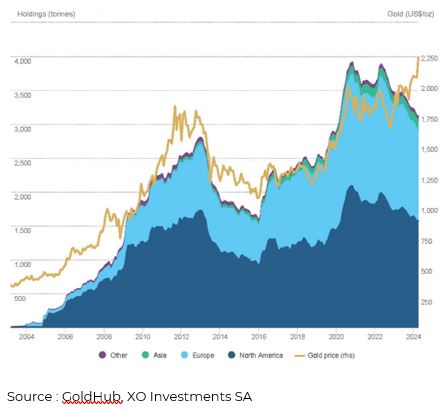

Asian flows contrast with the long-term picture of global gold holdings via ETFs. There has been a real divergence over the past 3 years, with assets falling as gold rises. This is a rare phenomenon that generally normalises, one way or the other.

Gold holdings (tonnes)

Current investor disinterest

In addition to divergence, a holding of gold that is falling while gold is rising also shows a degree of disinterest on the part of investors.

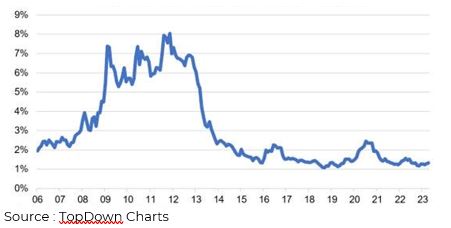

It is possible to determine an implicit allocation to gold in portfolios by calculating the proportion of assets invested in gold ETFs relative to the volumes of all ETFs. This method gives us a picture of an asset neglected by investors, with an allocation of around 1% in portfolios. This is a far cry from the 8% held on average in 2011.

Implied allocation to gold

By comparing the value of an equity index (S&P500) with gold, we obtain an interesting ratio of strength and weakness between the two assets. While equities were widely preferred in 1970 or 2000, gold was the preferred asset in 1980. We are now in a period of strength for equities against gold. This could lead to a normalisation and a greater appreciation of gold than equities in the future.

Ratio S&P500 / or

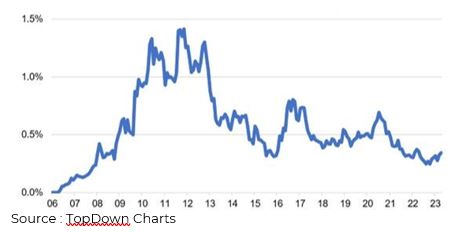

The implicit allocation to gold mines is even lower, representing just 0.5% of investors' portfolios, 3 times less than in 2011.

Implicit allocation to gold mines

Gold mines are undervalued relative to gold itself. The ratio between the two assets is at an all-time low, meaning that the price of gold mines has never been so low relative to the price of gold.

Ratio mines d'or / or

Everyone's talking about it, but few possess it

Gold is shining brightly at the start of this year, driven by central banks and Asian flows. But it is shining alone at the moment, with investors who are note positioned wondering whether they should buy it.. which should fuel potential future flows and prolong this movement.

These other articles may also interest you