Switzerland pays the price for its success

The SNB's surprise decision to cut interest rates before the other main central banks highlights the coutry's main problem : its prosperity.

What if Switzerland's prosperity was also its main problem? We can easily imagine this if we listen to exporters, who are penalised by the strength of the CHF, or investors, who have to make do with interest rates that are very low by international standards.

A flourishing economy

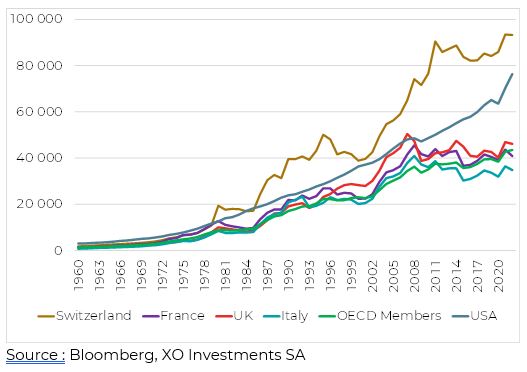

Despite its small size, difficult terrain and lack of raw materials, Switzerland has been competing with ingenuity for decades. The country has one of the highest per capita GDPs in the world. While living standards were comparable to those in France in the 1960s, per capita GDP is now twice as high as in France. Europe lags far behind, even though Switzerland is geographically embedded in it. Free-trade agreements with China and, more recently, India, mean that Switzerland is a bridge between several worlds.

GDP per capita (constant USD)

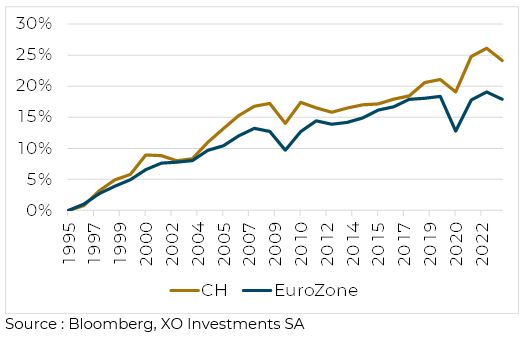

The country concentrates its activities in high value-added sectors. Labour productivity, already one of the highest in the world, is nevertheless rising steadily. High wages are therefore not holding back a flourishing economy.

Productivity growth

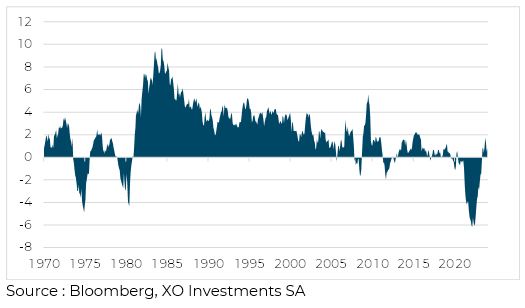

Legal certainty, political stability, multilingualism, tax attractiveness - so many advantages in a world that is becoming increasingly unstable. This stability is also reflected in prices, with an inflation rate well below that of its Western counterparts.

Swiss inflation (%)

The ransom of success

Low inflation is an undeniable strength for the Swiss economy, but it also reveals the other side of the coin: the strength of the currency. The strength of the CHF is beneficial for imports and helps to limit the inflationary impact of energy prices, for example, but represents a considerable burden for the export industry.

Both the EUR and the USD have lost an average of 3% of their value against the CHF over the last 50 years. Companies must therefore compensate for this 3% loss through higher productivity or better quality.

EURCHF

USDCHF

As a result, investors are being penalised, as each time they invest abroad they can expect the currency to fall by 3% a year. Investors are also affected locally on the bond market, since interest rates are lower than internationally.

The SNB takes action

After a year in 2023 in which the CHF appreciated by 9% against the USD and by 6% against the EUR, and once inflationary uncertainties had been dispelled, the SNB decided to take action in March 2024.

2-year rate CHF (%)

The decision to cut rates immediately came as a surprise to specialists, as it was so far ahead of the movements of other central banks, particularly the FED. The SNB is demonstrating its desire to control inflation while not allowing the CHF to appreciate too quickly.

Long-term interest rates (10 years) have remained stable and will only slightly affect the performance of bond indices.

10-year rate CHF (%)

The yield curve, symbolised by the difference between long-term rates and short-term rates (10 years - 2 years), remains relatively flat despite the SNB's decision. Time has virtually no value in the current configuration.

Differential 10-2 years CHF (%)

Real interest rates

The most interesting interest rate to watch in the current context is undoubtedly the real interest rate. This rate represents the difference between the nominal interest rate and inflation. A positive real interest rate means that holding a long-term government bond is positive because the return exceeds inflation. Conversely, a negative real interest rate leads us to conclude that the holder of a government bond is impoverished by inflation. On the other hand, this is the best scenario for the indebted government, since its debt is eaten away by inflation.

The real interest rate is the control point for central banks. In just a few months, Switzerland has managed to control inflation and return to a satisfactory situation of positive real interest rates.

Real rates CHF (%)

The situation is similar in the United States, where real interest rates have returned to positive territory. But the context is different on the other side of the Atlantic, since the level of US government debt is not comparable to that of Switzerland. Whereas negative real interest rates allowed the US to "forgive" its debt, positive real interest rates and deficits in both the trade balance and the government budget are plunging the US government into a debt race from hell.

US real rates (%)

These circumstances will inevitably lead to a fall in the value of the USD, particularly against the CHF, and thus to a new "ransom" for the Swiss economy. A virtuous or vicious circle is being set in motion for a country that has no shortage of ideas, but must constantly find new ones, or risk becoming... normal.

These other articles may also interest you