US Debt rises to the sky

The recent shutdown episode highlights the growing weight of us debt. The rotation of debt holders is accelerating in a context where the fed is the us government's largest creditor and China is de-dollarizing.

A debt that rises to the sky

There's a saying in finance that trees don't grow up to the sky. This adage seems to be wrong when it comes to US debt. The recurrent discussions on raising the debt ceiling in the U.S. federal chambers show just how central the debt issue is to the debate and to the U.S. economy.

The initial source of this debt is a double deficit (public deficit and current account deficit) that has been recurring for 30 years. Every year, the U.S. government not only has to roll over its debt, i.e. repay and then re-borrow, but also has to borrow more to pay off this deficit.

Double US deficit (% of GDP)

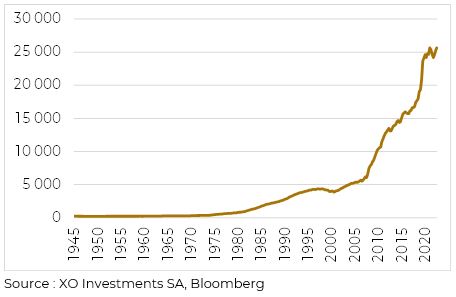

The obvious consequence is an increase in US government debt, with over USD 25 trillion in commitments. This rise became dizzying from the 2008 crisis onwards, and accelerated even further with Covid.

US debt (billions USD)

The FED as principal holder

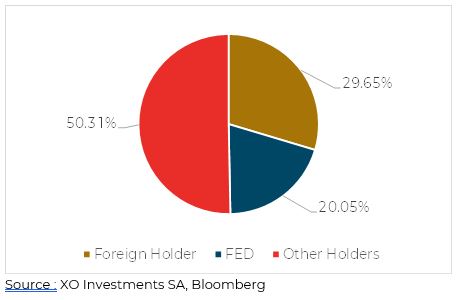

US debt is held by three types of players: the Federal Reserve, foreign governments and other holders.

Breakdown of US debt

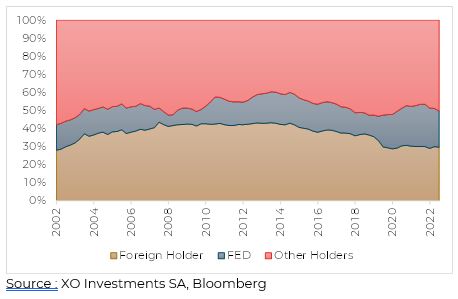

Over the past 20 years, the breakdown of holdings between these three debtholders has remained fairly stable, although the weighting held by the Fed has increased.

US Debt distribution

The "Debtholders" holding US debt are mainly large US banks or asset managers, who buy this asset for their bond or diversified investment funds, or to invest their own funds. The top 10 banks hold 10% of total US debt.

Other principal holders

China de-dollarization

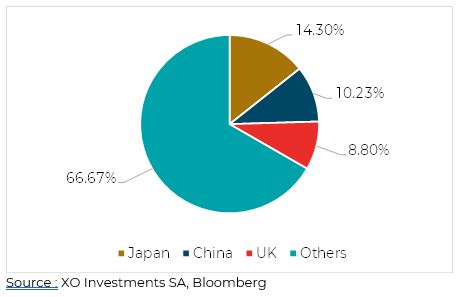

Foreign governments account for 30% of US debt holdings. This is a crucial point, because it has a geopolitical dimension. Holding U.S. debt means holding U.S. dollars, and therefore creating a link between two economies, or a relationship of dependence between one and the other.

Foreign holders

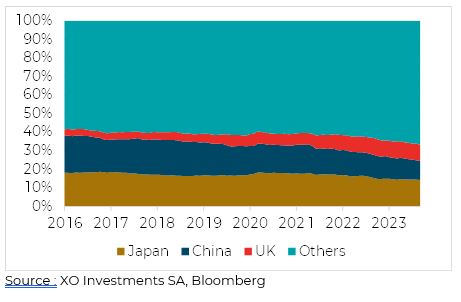

The three main holders are Japan, China and the United Kingdom. Recent trends are interesting, with the UK making progress, Japan remaining stable and China gradually reducing its weight.

Trend in major foreign ownership

This reduction dynamic is in line with the declarations of the BRICS countries, which are increasingly trading with each other in their national currencies, and their desire to stop using the USD. As a result, China chooses not to reinvest every time it is repaid US debt. It therefore sells USD to buy CNY, thereby reducing its exposure to the USD. China still holds 770 billion in debt, compared with 1,200 billion 7 years ago.

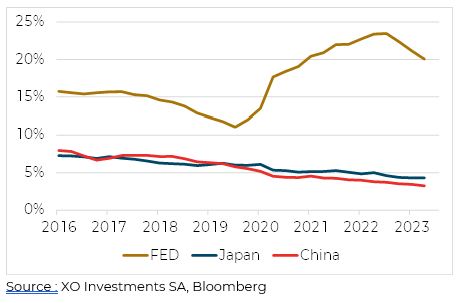

Nevertheless, the Fed remains the main holder of US debt, with 5 trillion in assets representing 20% of total debt.

Main holders (% of total debt)

When issuing US debt, the government is faced with weaker demand than in the past, as certain players, such as China, disappear from these auctions. As a result, other partners such as Great Britain are emerging, but this may also explain the upward pressure on US interest rates.

Approaching renewal deadlines

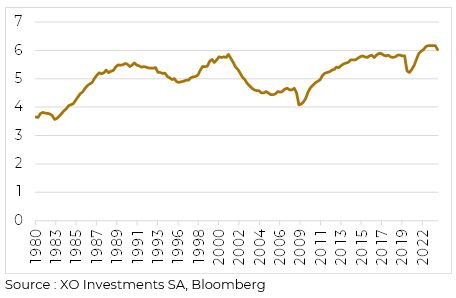

US debt has an average duration of around 6 years. In other words, all bonds issued by the US government have an average maturity of 6 years. This value has risen over the past 40 years as interest rates have fallen.

Duration of US debt

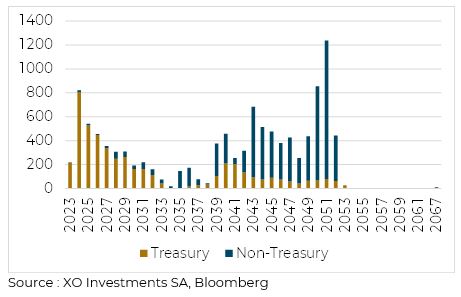

An analysis of the US debt maturity distribution shows that 40% of this debt matures within 3 years. The 6-year duration is the result of the very long maturities of part of the debt, peaking in 2053. With 40% of debt maturing quickly, the average cost of borrowing is likely to rise with current interest rate levels. As a result, the budget deficit will rise, and the government will have to borrow even more to finance the deficits. A vicious circle is gradually taking shape.

Maturity of US debt (trillions USD)

The Fed is likely to be called upon to help. Its intervention would make it possible to maintain a high level of debt without suffering too much from the disappearance of certain US government creditors (China, Russia, etc.). The Fed has a relatively similar profile in terms of the distribution of US debt in annual terms..

Maturity of FED portfolio (USD billion)

Although the Fed has been independent of the US Treasury Department since its creation in 1913, it remains the largest holder of US debt, and is likely to increase its importance still further. For the time being, these inbred links, which run counter to the basic principles on which the Fed was founded, enable the US government to raise the debt ceiling step by step, and to continue using the US dollar as a vehicle for economic domination.

These other articles may also interest you