From« Too Big to Fail » to « Too Huge to Collapse »

The takeover of Credit Suisse by UBS raises many questions about the banking system, which is synonymous with concentration, leading to the creation of ever larger players. Autopsy of a death

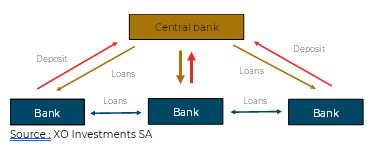

Central banking systems

More than a century ago, the central banks of Western countries were born. The SNB was created in 1905, the FED in 1913. The latter was set up following several banking crises in the United States. Its role has of course evolved over time but its initial objective of independence and guaranteeing monetary stability is obviously the key to its existence. For more than a year now, central banks have been concentrating on the fight against inflation. They have two tools at their disposal. The first is obviously the level of interest rates. This is the easiest to understand. The second is the control of the money supply via the possible lending by commercial banks.

Functionning of central banks

The central bank system is based on the following principle: commercial banks deposit part of their assets with the central bank and can then lend money by creating it. A leverage (or multiplier) is then created. Indeed, the money from a client's deposit will allow the creation of X times more loans (10 for example), which will in turn be deposited in another bank which will be able to lend, and so on. The multiplier X depends on the reserve ratio that the commercial bank must deposit with the central bank. It is therefore not the central bank that creates the money from credit (mortgage or commercial) but the commercial banks. This lending activity is necessary for a healthy economy where the supply of finance matches the demand for finance.

A traditional commercial bank, as Credit Suisse was, can thus lend to individuals or companies on the basis of deposits it holds for other individuals or companies. The only constraint is that it must deposit reserves with the central bank.

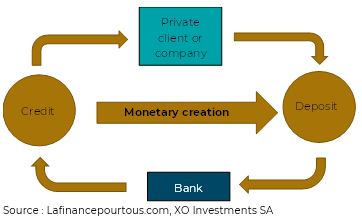

Commercial money creation

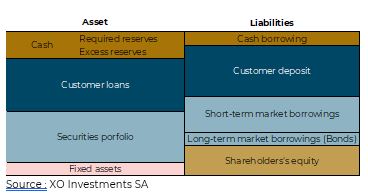

A healthy balance sheet

A bank's balance sheet can thus be summarised as follows. A bank's assets consist of cash, loans to private and corporate customers, market positions and fixed assets such as buildings. The bank's liabilities include cash borrowed from other banks, customer deposits, the bank's bonds and equity, i.e. shares.

Balance sheet of a bank

The more customer deposits and equity the bank has, the more it can lend. This money creation can be unlimited. The only constraints are set by the central bank with mandatory deposits. These are in particular the solvency ratios.

Credit Suisse, for example, had a Common Equity 1 ratio of 14.1%, which is above the required level of 10.6% in Europe. This ratio measures the ratio between the bank's equity (capital + reserves) and its assets (loans, market positions). The second ratio used is the "liquidity coverage ratio", a measure of the level of liquid assets to cover 30-day needs. This ratio was 150% before the collapse, which is above the minimum requirement of 100%. So all the solvency ratios were in the green for Credit Suisse in financial terms, suggesting that it was not a major risk.

Loss of confidence

So how did this happen? Simply because Credit Suisse was not just a deposit bank, it was also an investment bank. An investment bank owes its performance to the performance of the financial markets and the commissions it earns on trading and stock market activities, for example. The commercial bank owes its performance only to the demand for credit and thus to the interest rate margin. And it is in this area of investment banking that Credit Suisse has unfortunately experienced a number of problems in recent years: Archegos, Greensill, Tuna Bonds from Mozambique, ...

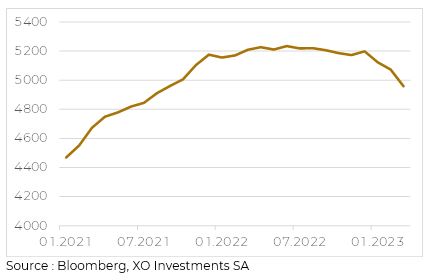

These various problems have led the bank to announce massive losses. Even though they were largely bearable, confidence deteriorated and the share price only fell. Confidence disappeared progressively, at the same rate as the equity capital, since the share price represents a part of the equity capital, the whole credibility as a lender, and therefore as a deposit bank, was affected.

Evolution of the Credit Suisse share

Bigger and bigger banks

The consequence of the gradual loss of confidence in Credit Suisse is obviously the transfer of assets to other banks. This was also the case with the failure of the SVB bank in California. And the movement is still the same, clients go to bigger banks, to ensure protection through the "Too Big to Fail" mechanism. This is confirmed in the figures, deposits at small US commercial banks are falling sharply in favour of the larger ones.

Other deposits of small US commercial banks (billions USD)

In the Swiss case, the Federal Council even chose not to use the "Too Big to Fail" safeguard plan in order to move even faster and thus preserve confidence in the Swiss financial centre. This will create an even bigger UBS, which will have to separate all the activities of the former Credit Suisse and restructure its own bank.

The consequence of this crisis on the central banks is also major, since after more than a year of reducing their balance sheets, the central banks have had to change their policy and provide the market with gigantic liquidity. The SNB provided CHF 100 billion and the FED nearly USD 350 billion. The FED continues to raise interest rates but has just shown the market that it is ready to intervene in the event of a problem in the banking system.

Weekly growth of the FED's balance sheet (millions USD

In the Swiss case, the Federal Council even chose not to use the "Too Big to Fail" safeguard plan in order to move even faster

Towards a " Too Huge to Collapse"

The takeover of Credit Suisse by UBS shows how the banking system has become so interdependent and colossal that it requires total reactivity and huge amounts of money to stabilise the system. Central banks, independent of states, needed major political decisions to curb the crisis. In other words, central banks without political power would have been unable to calm the situation. The system therefore ends up in the opposite situation of the creation of central banks, which were supposed to be totally independent of governments.

The banks will therefore become ever larger as crises and regulation continue to increase. Central banks will also become ever larger and ever more linked to governments. Liquidity injections will resume for a market addicted to the easy money of recent years.

"You don't solve a problem with the same thinking that created it’’. A. Einstein.

Ces autres articles peuvent également vous intéresser