Swiss Bonds : Chasing Lost Yields

This massive fall in the Swiss bond index in 2022 has one positive consequence : it gives a new lease of life to an asset class that has long been reviled by investors because its yield is too low, or even negative !

An asset under pressure

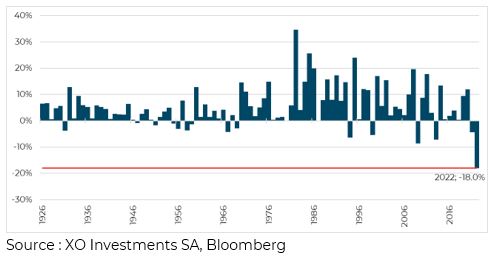

The year 2022 swept away conventional investment wisdom: in periods of turmoil on the equity markets, bonds traditionally tend to cushion the blow by offering a decorrelated return. Last year failed to conform to this wisdom. In fact, the opposite was true, with the bond market, like the US market, posting its worst performance ever.

Performance of US bonds

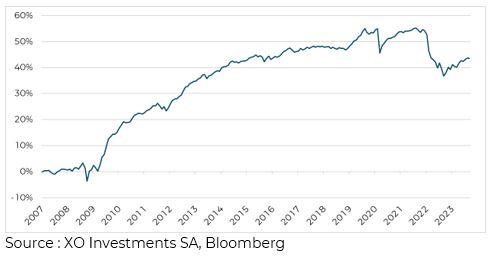

Swiss bonds are no exception, despite their defensive nature. Almost 10 years of performance have evaporated in the space of a year.

Performance SBI AAA-BBB

The reason for this sudden movement is obviously interest rates and the high duration of the index (duration measures the sensitivity of the value of a bond to interest rate movements). With 10-year yields rising by around 2%, given the duration of the index, which exceeds 7, the performance is logically 2% * 7 = 14% down. Mathematical logic is respected... but investors' feelings are put to the test.

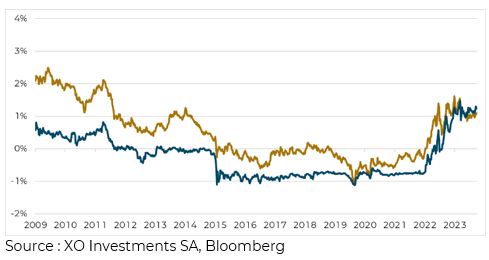

Rate 2 and 10 years CHF

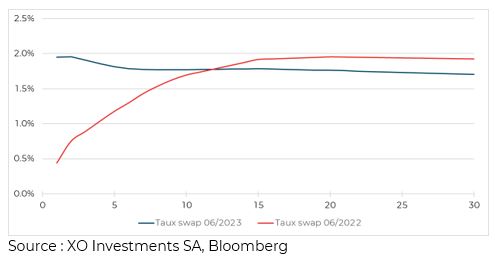

For a year and a half now, the interest rate curve has changed radically. Throughout the first half of 2022, it was the long end of the curve, i.e. maturities in the distant future, that saw interest rates rise in response to investor expectations. From the second half of 2022 onwards, it was the short end of the curve, i.e. maturities in the near future, that saw interest rates rise as a result of rate hikes by the central bank. As a result, the yield curve has flattened out completely, moving from the red curve in June 2022 to the blue curve in June 2023. This curve is even slightly inverted, signalling a recession. This inverted curve is not uniquely Swiss , as the US and European curves were also inverted for most of 2023.

Rate curve CHF

A more buoyant market in the future

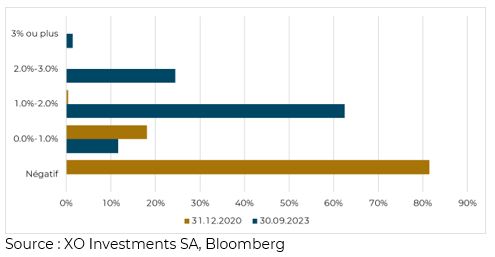

The cataclysm of 2022 had not only negative effects. Three years ago, most bonds on the market (over 80%!) were trading at negative yields. Today, not a single bond has a negative yield and 60% of the bonds in the index have a yield to maturity (YTM) of between 1% and 2%. The market is healthier and back to where it was before the period of negative rates, i.e. before 2015.

SBI by YTM

The cataclysm of 2022 had not only negative effects. Three years ago, most bonds on the market (over 80%!) were trading at negative yields. Today, not a single bond has a negative yield and 60% of the bonds in the index have a yield to maturity (YTM) of between 1% and 2%. The market is healthier and back to where it was before the period of negative rates, i.e. before 2015.

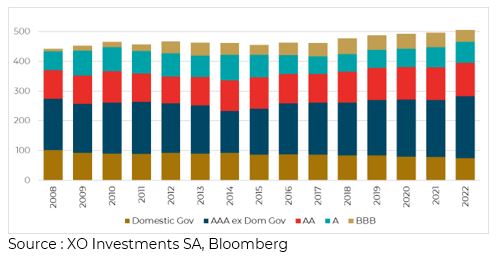

Composition of the SBI Index (CHF bn)

Favouring the investments-grade credit segment

In Switzerland, companies are increasingly financing themselves on the bond market. This offers investors not only better diversification but also higher returns. Over a 16-year period, the cumulative difference between the traditional SBI index and the SBI BBB is 15%.

Cumulative performance

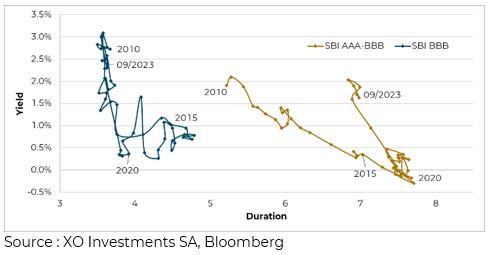

The profile of the SBI BBB index is also interesting in terms of risk/return ratio, since it has a duration 4 years shorter than the SBI AAA-BBB, so less risk in the event of a rise in rates, but also a higher yield to maturity.

Yield vs duration

The complete breakdown of index returns, including default risks in the credit segment, is to the advantage of an investment in BBB ratings. It is even possible to simulate the return on this Investment Grade credit segment, based on the probability of default and a recovery rate in the event of bankruptcy. All the yellow and green sections of the table below present scenarios favourable to a credit investment instead of an investment in the global market. With the exception of a few rare possibilities, everything suggests that it is the credit segment that should currently be favoured.

Return on Risk

Swiss bonds as the basis of a portfolio

Swiss bonds have always had a defensive profile for investors, although 2022 is the exception that proves the rule. The rise in interest rates is now enabling investors to regain the returns they lost during the period of negative interest rates. The 'credit' part of the index offers a very attractive risk/return profile, and should enable investors to gradually reposition themselves in an asset class that few considered just a few months ago. Swiss bonds could simply once again become the basis of a Swiss client's portfolio, thereby financing the growth of Swiss industry. Or how to kill two birds with one stone!

Ces autres articles peuvent également vous intéresser